General Information

Subject Area: Mathematics (B.E.S.T.)

Grade: 912

Strand: Financial Literacy

Date Adopted or Revised: 08/20

Status: State Board Approved

Benchmark Instructional Guide

Connecting Benchmarks/Horizontal Alignment

Terms from the K-12 Glossary

Vertical Alignment

Previous Benchmarks

Next Benchmarks

Purpose and Instructional Strategies

In Math for Data and Financial Literacy, students explore different strategies to pay off debt.- Instruction begins with planning to pay off a single debt then moving to paying off multiple debts within a personal budget plan.

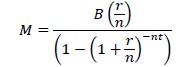

- Calculating the monthly payment needed to pay off the credit card in a specified amount of time requires a new formula. (Note: there are several websites that provide calculators that use this formula as well.) In the formula below, is the existing credit card balance, is the monthly payment, is the interest rate expressed as a decimal, is the number of times the interest is compounded annually and is the length of time in years.

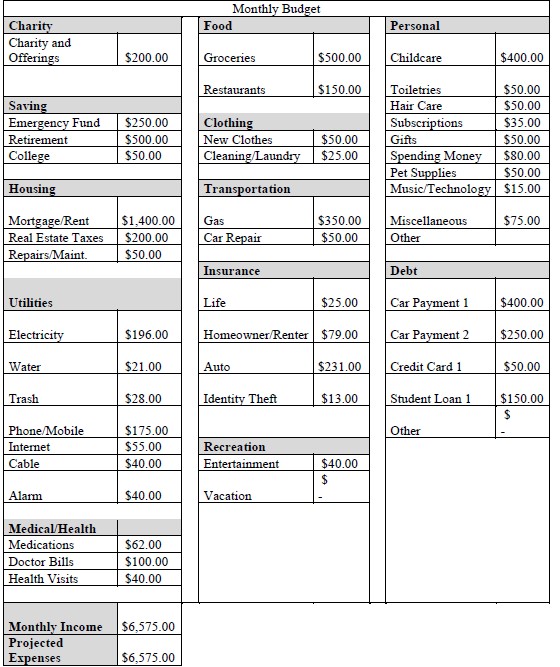

- After students have calculated monthly payments needed to pay off debt in a desired timeframe, they will need to devise a plan in their monthly budget to allocate the necessary amount for debt reduction. Provide sample budgets like the one below and have students discuss (MTR.4.1) what changes could be made to make room for new debt, reducing debt or other adjustments.

- As students discuss, guide them to recognize a few key points like some categories in the budget are easier to adjust (i.e., entertainment or restaurants) than others (i.e., mortgage or electricity).

- Instruction includes prompting questions that allow students to discuss various situations that may arise within trying to establish pay off plans.

- Even when establishing a payoff plan, why might it be good to maintain an emergency fund?

- What additional expenses might occur during your payoff plan?

- What are some ways you might increase your income temporarily to help pay off debt faster?

- How could your budget differ if your only debt was your mortgage?

- Instruction includes making the connection to long-term retirement savings when deciding to reduce retirement funds for a payoff plan. Guide students to explore the Periodic Investment formula using a spreadsheet and a cell reference for the monthly contribution (which allows students to change it easily) to allow students to quickly see the exponential effects of reducing their monthly retirement savings.

- Instruction includes exploring various time frames when determining a payoff plan.

- For example, monthly payments of $412.56 may be required to pay off a card in a year. Have students determine if adjustments to the budget be made to achieve this.

Common Misconceptions or Errors

- Given the complexity of the formulas used in this benchmark, be sure to calculate one example by hand and by technology to confirm any formulas entered into spreadsheet technology are calculating correctly.

- When using spreadsheet technology for analysis, multiple problems can develop as students create and enter formulas for calculations. Write sample formula entries (i.e., the credit card payoff formula=(4500∗(0.18/12))/(1−(1+(0.18/12))^(−12∗3)) on the board for them to emulate to help prevent this. Note that many programs require a ∗ symbol to denote multiplication. Placing two variable (or cells) side by side may generate a REF error.

Instructional Tasks

Instructional Task 1 (MTR.6.1, MTR.7.1)- You and your spouse are working on reducing your debt. You recently received a raise that increases your take home pay by $600 per month. Your current debts (outside of your mortgage) are listed below.

- Part A. Would this extra income allow you to pay off these debts in four years, assuming no additional debt is incurred?

- Part B. Compare the impact of paying increased payments for all three debts simultaneously versus focusing all the additional income on the smallest debt first.

- Part C. How quickly could the smallest credit card be paid off? How long until the next card is paid off (consider the current monthly payment for card 2 could be applied to card 1 once card 2 is paid off)?

- Part D. How long until the student loan is paid off?

- Part E. Describe the benefits of paying off smaller debts first.

Instructional Items

Instructional Item 1- Jacqueline has a car loan she wants to pay off early. The loan is at 2.99% APR and has a current balance of $17,653.28. She currently makes a car payment of $387 each month. After paying off two of her credit cards, Jacqueline determines she could pay an additional $150 per month toward the car. Will this increased monthly payment allow her to pay off the car in 3 years? Why or why not?

*The strategies, tasks and items included in the B1G-M are examples and should not be considered comprehensive.